How To Manage Your Money: Tips To Do It Right

Even though money isn’t the only thing buying you happiness, money can help you gain resiliency. Unless we take control of money, we can never be sure if it's going to happen in the future or achieve financial security.

The study showed 37% of Americans use credit cards if there was an economic crisis of $1,000 in the past two years - or even less.

Even worse, people are using their credit cards to cover their everyday expenses and are barely making minimum payments to their credit cards. Sometimes, they are even missing their payments, derailing, even more, their financial life.

You really want to avoid this situation but this will require knowing how to manage the money. In this article, you will learn how to manage your money along with some tips to do it right!

How To Manage Money

There are a few key things that you can do in order to manage your money more effectively. First, you need to make sure that you have a clear understanding of your current financial situation. This means knowing how much money you have coming in each month, as well as what your regular expenses are. Once you have this information, you can start to create a monthly budget.

Creating a budget is especially important if you have credit card debt or other loans that you are trying to pay off. Once you have a budget in place, you can start to look for ways to reduce your expenses and save money.

One important aspect to manage your money is to learn to control your spending, you will be able to free up more money to save or to put towards paying off debt.

Another important aspect of money management is investing. When you invest, you are putting your money into something that has the potential to grow over time. This can be a great way to build your wealth and secure your financial future. There are many different types of investments available, so you will need to do some research to find the right one for you.

How do I manage my money?

There isn't a better way to Managing Money than now. How do we manage our money? CoVID19 has impacted the US economy in many ways. Scores of workers have departed their jobs for the 'Greatest Resignation', while other employees opt for a temporary, remote working schedule.

While prices rose for homes and land in the suburbs, some families purchased a new home. Others moved their children into private schools or started homeschooling when viruses exploded and they were infected.

Start an Emergency Fund

One of the most important steps you can take to manage your money and personal finance is to start an emergency fund. An emergency fund acts as a buffer against unexpected expenses or income shortfalls. It can help you avoid going into debt or selling off investments in a down market.

There are a few different approaches you can take to starting an emergency fund. One option is to set aside a fixed amount of money each month. Another approach is to save a percentage of your income each month. Whichever method you choose, the important thing is to start building up your emergency fund as soon as possible.

If you're not sure how much to save, a good rule of thumb is to aim for three to six months' worth of living expenses. However, you may want to save more if you have a volatile income or large expenses, such as a mortgage or medical bills.

Once you've decided how much to save, open a separate account and make regular deposits. Many banks offer high-yield accounts that offer higher interest rates than traditional accounts. This can help you grow your emergency fund even faster.

With a little planning and discipline, you can soon have a healthy emergency fund to protect you in case of unforeseen events.

Bank Account

When you manage your money, one of the things you'll need to do is open a bank account. This will help you keep track of your spending and saving, and it can also be a convenient way to pay bills and make other financial transactions. There are a few different types of bank accounts, so it's important to choose the one that's right for you.

The most basic type of account is a checking account. This is the account you'll use to deposit your paycheck, pay bills, and make everyday purchases. You can usually write checks or use a debit card linked to your account to make payments. Checking accounts typically don't earn interest, but they may offer other perks like ATM access and online banking.

If you're looking to save money, a savings account may be a good option. This type of account typically earns interest, so your money can grow over time. Many banks also offer special accounts, like certificates of deposit (CDs), which offer higher interest rates in exchange for keeping your money in the account for a set period of time.

If you're interested in investing, you may want to open a brokerage account. With a brokerage account, you can buy and sell stocks, bonds, and other investments. Brokerage accounts typically have fees and commissions associated with them, so it's important to do your research before choosing one.

Savings Account

Saving money is one of the most important aspects of managing your finances. By setting aside money each month, you can ensure that you have funds available for unexpected expenses or for goal-related purchases. Savings accounts offer a safe place to store your money, and many banks offer interest rates that can help your savings grow over time. When it comes to saving money, it’s important to create a plan that works for you and your unique financial situation. Start by evaluating your income and expenses to determine how much you can realistically set aside each month. Then, choose an account that offers features that align with your goals. Whether you’re looking for a high-interest rate or easy access to your funds, there’s an account that’s right for you.

Understand your current financial situation

Before you can make any more financial decisions you should look into what is happening to you. You have to know where your wealth will go. If you need to understand what is happening financially, you will need a record of your monthly and annual earnings. Heider says there are numerous applications that automate the entire workflow. Mint Pocket Guard and Quicken Simpleifi are several free app options. The free app allows a simple synchronization of financial information into one's financial account.

Pay off debts

Getting into debt may cause a lot of difficulties, but it's also a challenge to repay them. As the majority of debts earn interest the debt can take time. The most efficient way to repay a debt is by focusing if possible on the debt. Once that is paid off you can transfer the payments to the next loan and proceed until the debt has been cleared. In some situations, this can be helpful when consolidating high-interest credit cards into lower-interest credit card loans. The debt settlement option only works in the event a person commits to a lifestyle in the future in a sustainable way, based upon their incomes and needs.

Set personal priorities and financial goals

If you are unsure of the way in which your current situation matches your values then you can begin to evaluate. There's just no purpose to your day. There are several things that are important to us. Having clear goals can help you create an effective budget more quickly. When it comes to family vacation time, paying to have a housekeeping service might help cut the costs. Obviously, traveling will be more important for people. In such cases, the amount of housekeeping money might be better used during the holidays. When determining financial goals one often makes the mistake of limiting himself.

Learn Self-Control

Hopefully, your parents taught you the skill of self-control as children. Hopefully, you're able to avoid the hassle of wasting money by not doing it. Although you can easily purchase an item with credit when you want it, you should wait until you have saved enough funds. Can we afford the interest in our jeans and cereals? Debit cards are also very useful because they take money out of your bank account simultaneously keeping the balance free.

Create and stick to a budget

Writing a plan to plan your income for the upcoming months is simple. But achieving them can sometimes pose difficulties. It might be difficult or even impossible for some of these individuals to restrict their purchasing impulses.

Having extra money available on a budget can be a great reward. A budget written with the right objectives can be easily followed. When you see that you do not have the money for anything else you would prefer, find ways to cut down costs.

Know where your money goes

If you look at your financial statements you will realize the value of keeping your expenses under control without exceeding the income. This can happen through budgets.

As soon as you realize that your coffee costs will rise monthly, you will realize that reducing your spending can have the biggest impact on gaining the raise. As an additional benefit, it’s easy and inexpensive to reduce your monthly recurring costs. It's like finding free money!

What is the 50 20 30 budget rule?

The 50 20 30 budget rule is a simple way to manage your finances. The rule states that you should spend 50% of your income on essentials, such as housing, food, and transportation. 20% should be saved for future goals, such as retirement or a rainy day fund. And 30% can be spent on discretionary items, such as entertainment or travel.

This budgeting method can be a helpful way to keep your spending in check and ensure that you are saving enough for your future goals. However, it is important to remember that everyone's financial situation is different and there is no one-size-fits-all approach to budgeting. If the 50 20 30 rule doesn't work for you, there are other methods you can try.

Follow the Baby Steps

If you want to reach your financial goals, you must find a plan that shows a clear course. The good news is our money-management system will work for you: Dave Ramsey's seven-step guide. Your company is trying to eliminate the sleazy consultant from your team. Explore the best professional investment advice for you! It has helped thousands escape debt to build wealth. It is based upon a proven financial model. Tell me about the first step of the parenting journey? It was really fun getting your responses! If you can keep your eyes open to something, you're going to make real progress.

Schedule regular progress reports

Management of a business's finances requires constant effort. This helps schedule regular times for you to evaluate the state of your finances and your financial assets. You can review your credit report annually by requesting a copy of your Annual Credit Report online to identify errors and potential fraud which can negatively affect the rate you pay for your credit card as well as your bank account.

Save and invest for your future

Here's where it starts to get exciting. We have to focus on pursuing our futures! Despite many people believing investing is their top financial goal, the reality is there is still some work in progress.

According to the US government, the number of people saving for retirement has doubled from 42 percent to 44 percent of those who have saved. America needs to put things right. It can be difficult to change the course of your life despite how little your egg contains. No age limit to get started. Retirement is about to happen.

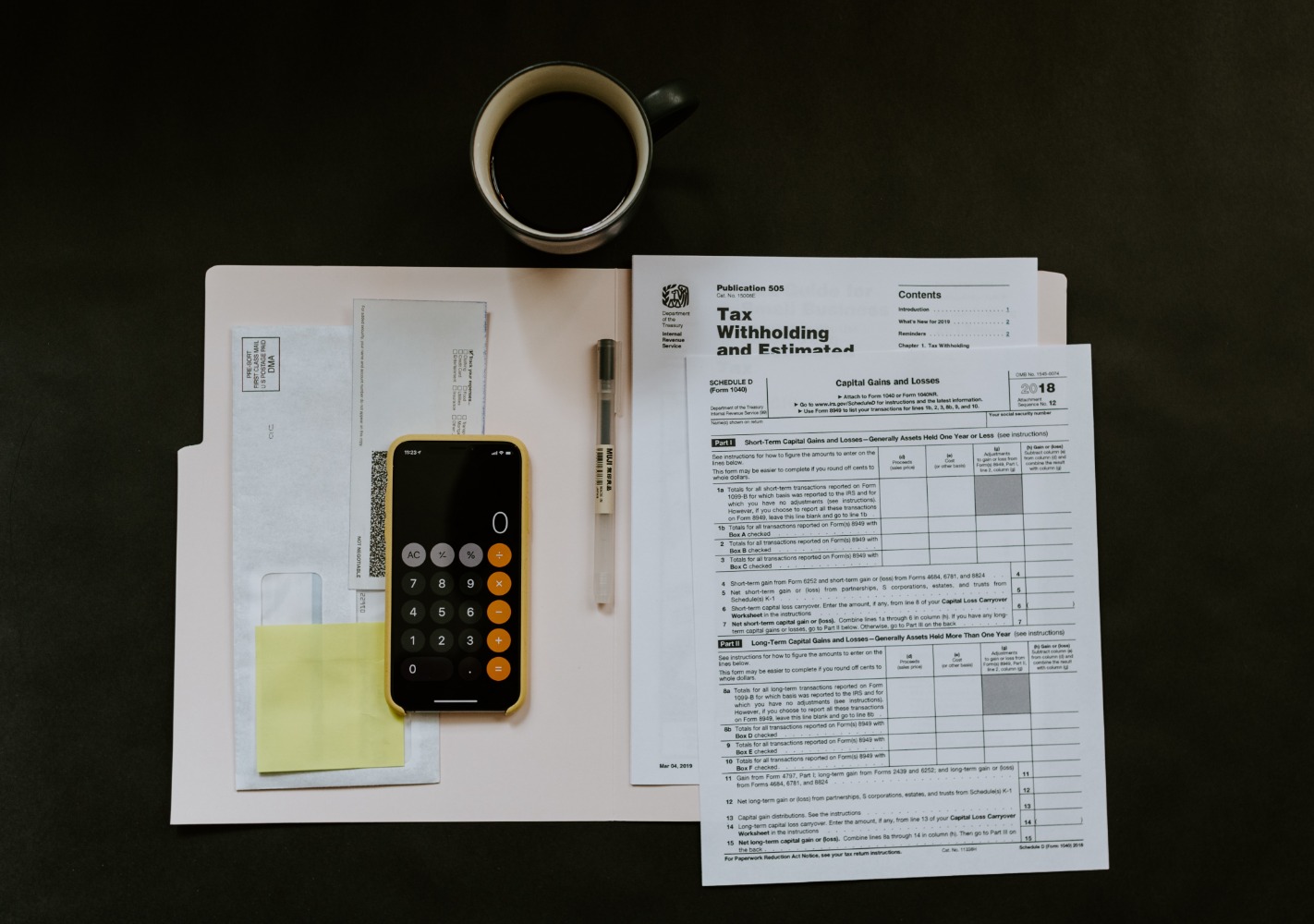

Get a grip on taxes

Taxation is a big problem for everyone before the first paychecks come in. When an employer provides you with your salary information, they will show you your gross income, and your after-tax dollars will be.

Many payroll tax calculator websites are available that simplify the calculation of payroll taxes like PaycheckCity. This calculator enables you to calculate, based on your monthly income, your gross salary as well as the income tax amount you have, also called net or take-home wages.

Save for retirement

When you retire, you will not have the same income as you did when you were working. You will need to make sure that your retirement savings are enough to cover your costs. There are many ways to save for retirement, but one of the most common is through a retirement account.

Occasionally we need retirement. It takes time without retirement funds. Social Security benefits do not replace about 50% of your salary. Several employers no longer offer pensions. People focus too much on debt and forget to retire,” he adds. You have to start thinking about retiring soon.

Worker retirement plan plans, like a 401k account, are a useful way to save money for retirement because their contributions are automatically deducted from the salary of employees. Plus, employers could match the contributions of employees to increase retirement savings. This account may also have tax liabilities.

Retirement account

A retirement account is an account that is specifically for retirement. The money in the account is not taxed until you withdraw it, which means that it can grow more quickly than if it were in a regular savings account. There are many different types of retirement accounts, but some of the most common are 401(k)s, mutual funds, and IRAs.

Regardless of the instrument you choose, make sure they are aligned with your retirement savings goals. If you consider it necessary, consider hiring a financial advisor or setting up a Robo Advisor.

A certified financial planner is a type of financial advisor who helps people save for their future. They work with clients to create a budget and investment plan that will help them reach their financial goals. Certified financial planners often have a background in accounting or finance, and they use this knowledge to help their clients make the best decisions about their money.

Continue reading

When a person steps out of work, the most comfortable thing they can do will depend on how comfortable you feel at home. How one spends their retirement money also carries a major impact. Saving to retire is divided between the amount of stock money and the amount in bonds.

The stock market is volatile, sometimes, though it has traditionally delivered higher returns than the bond market over longer periods. Bonding is colder. They never fall in the same way stocks do, they usually go down as stocks collapse. Nevertheless, these stocks gain no more than stocks.

Protect your wealth

If your hard-earned cash goes bad you must take the necessary measures. Tell me the most important factors to take into account when you rent out an apartment or have it insured against theft. Please review policies for coverage and non-coverage. Disability insurance protects your greatest assets if it means you will have a stable income should your condition or disability prevent your job.

Money Management System

Assuming you have a regular income, one of the best ways to get in control of your personal finance is to create a money management system that tracks your spending. Do it for at least one month. This will give you an idea of where your money goes and help you identify any areas where you may be able to cut back.

There are many ways to track your spending, but one of the simplest is to use a notebook or create a spreadsheet to record every purchase you make during the month.

Be sure to include not only the amount spent but also what the money was spent on. At the end of the month, review your spending and see where most of your money goes.

There's no magic answer when it comes to how to manage your money so you have enough money to live on – it depends on your individual circumstances. However, we have introduced you to some basic steps you can take to get started in the journey of your financial success.

Control your financial future

If we don't know how we manage our finances, others can mismanage them for us. Many are ill-intentioned and may be unscrupulous financial planners.

Others may be well-intentioned, though may be unaware of what it takes. Instead of trusting someone else's guidance, read some of the basics of personal finances yourself.

To have a healthy financial future, you want to be in control of your money. This means learning how to budget, save, and invest your money wisely. It also means being mindful of financial risks and knowing how to protect yourself from them.

There are a lot of different ways to approach personal finance, but the basics always remain the same.

The bottom line

Remember it takes a few special training years for someone to be able to manage money effectively. How can you become financially prosperous as someone with a good financial management degree?